Car buyers overcharged £1,000 by dealers for loans, says watchdog

- Published

- comments

Some car buyers are being overcharged by more than £1,000 when they take out a loan to buy a car, the UK's financial watchdog has warned.

The Financial Conduct Authority (FCA) said the industry practice of allowing dealers to set their own interest rates was costing consumers £300m a year.

Dealers overcharge to boost their commission, the FCA concluded.

But the Finance and Leasing Association said the watchdog's survey was "based largely on out-of-date information".

Conflicts of interest

The regulator launched its investigation into the car finance market in April 2017 after there was a rapid surge in consumer credit led by car dealership finance.

At the time, it said it was concerned about a lack of transparency and potential conflicts of interest.

In its final findings on motor finance, external, the FCA concluded that the widespread use of commission models, which allow brokers discretion to set the customer's interest rate and thus earn higher commission, can lead to conflicts of interest that are not controlled adequately by lenders.

It said the practice can lead to customers paying significantly more for their motor finance.

Jonathan Davidson of the FCA said: "We found that some motor dealers are overcharging unsuspecting customers over a thousand pounds in interest charges in order to obtain bigger commission payouts for themselves.

"We also have concerns that firms may be failing to meet their existing obligations in relation to pre-contract disclosure and explanations, and affordability assessments.

"This is simply not good enough and we expect firms to review their operations to address our concerns."

Problem finance?

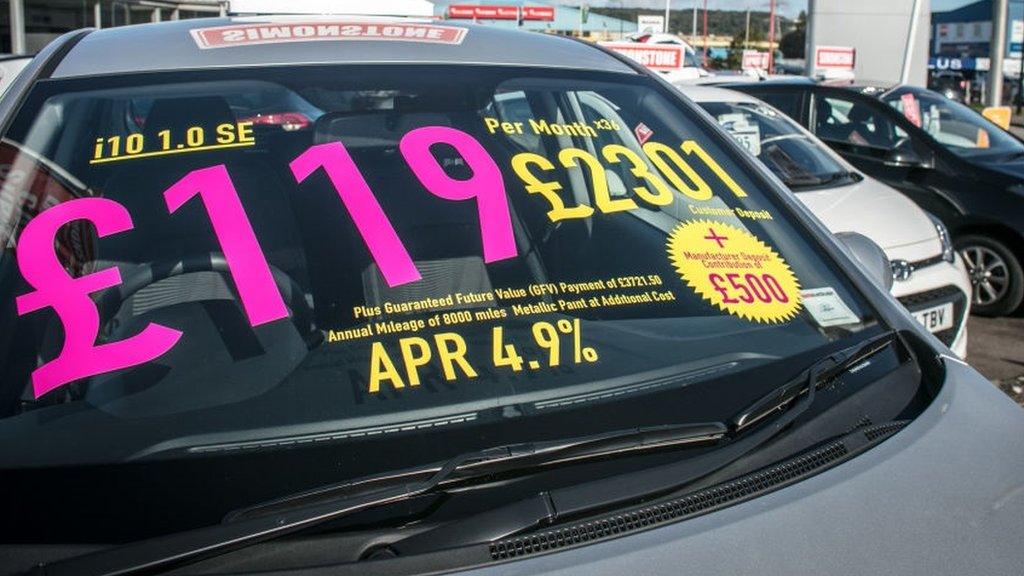

Four-fifths of new car finance deals are now what are known as Personal Contract Purchase, or PCP.

Instead of buying a car outright, a PCP allows consumers to effectively rent a car over a three or four-year period.

At the end of the period consumers can buy the car for its residual value (known as a "balloon" payment), hand the car back, or roll over the residual value into a new PCP on a new vehicle.

But problems have arisen because lenders have allowed brokers to set interest rates on the PCP agreements.

The FCA estimated that on a typical motor finance agreement of £10,000, higher broker commission can result in the customer paying around £1,100 more in interest charges over a four-year term of an agreement.

'Considerable progress'

The FCA said it was assessing the options for intervening in the market.

Options include strengthening existing rules or other steps such as banning certain types of commission model or limiting broker discretion.

In the meantime, the regulator said it would deal with individual firms where problems were identified, but it expects all lenders and brokers to review the way they do business to make sure they comply with the law and treat customers fairly.

The Finance and Leasing Association (FLA), a UK trade body for asset finance, consumer finance and motor finance, said that the FCA's survey work was "based largely on out-of-date information, and therefore does not reflect the very considerable progress the market has already made in moving away from such structures".

The FCA analysed contracts between lenders and dealers from 2013 to 2016 and examined lenders' data from January 2017 to July 2018.

The FLA added: "We look forward to working with the FCA as it modernises its regulations in line with market best practice."

- Published4 March 2019

- Published7 January 2019

- Published21 April 2017